* The views expressed in this article are the authors’ own and do not necessarily represent those of their organisations

In June 2019, the Montenegro Customs Administration (MCA) implemented a new Customs clearance procedure that uses pre-arrival data to fast-track Customs clearance of express cargo. Within just a few months, this pre-arrival processing (PAP) system enabled the MCA to improve its capability significantly, allowing it to clear parcels within one hour of arrival. Inspired by the project’s success, stakeholders wanted to gain a deeper understanding of how the improvements in performance had been achieved. They also wanted to find out whether any general lessons could be drawn for the purpose of assessing Customs performance. The findings of the ensuing impact assessment, conducted from April to October 2020, were recently presented at the WCO PICARD Conference 2020. This article provides a brief summary of those findings.

Highlights

⇒ The impact assessment identified several useful quantitative key performance indicators (KPIs). Apart from the faster clearance rate, other useful KPIs analysed during the assessment included efficiency gains and Customs’ increased hit rate, as well as cost savings and the express operator’s ability to make improvements to its service guarantees to the benefit of shippers.

⇒ The structured analysis of stakeholder needs yielded further insights in terms of assessing individual stakeholders’ strategic objectives and subsequent expectations regarding the procedure being implemented. The methodology of the assessment consisted, to a large extent, in learning and in building trust among the key stakeholders, which in turn achieves a greater impact and helps ensure a positive trajectory for the future.

⇒ The new methodology developed during the assessment could potentially be applied to other trade facilitation measures as well. Key elements include mapping stakeholders’ needs, clustering these needs into main themes and identifying corresponding KPIs.

⇒ The assessment’s results and methodology could potentially make a contribution to the ongoing work on Customs performance measurement.

The new PAP procedure

Montenegro’s pre-arrival processing procedure was developed as a project with the German Alliance for Trade Facilitation and piloted in collaboration with DHL (see Box 1). It currently allows authorized express parcel operators to submit an electronic import declaration in advance, prior to the arrival of the aircraft. The data is declared in a consolidated format and is used by Customs for risk assessment and Customs clearance. At present, the PAP procedure cannot be used to clear goods whose import requires licensing before or after arrival in the country.

The implemented PAP procedure is a significant departure from the pre-existing paper-based control system. At the time of concluding the assessment, 7% of all of the country’s imports were handled using this procedure. Data from DHL show that the rate at which parcels are cleared within 1 hour of landing has improved from 25% in 2015 to 53% in 2019.[1]

Impact assessment

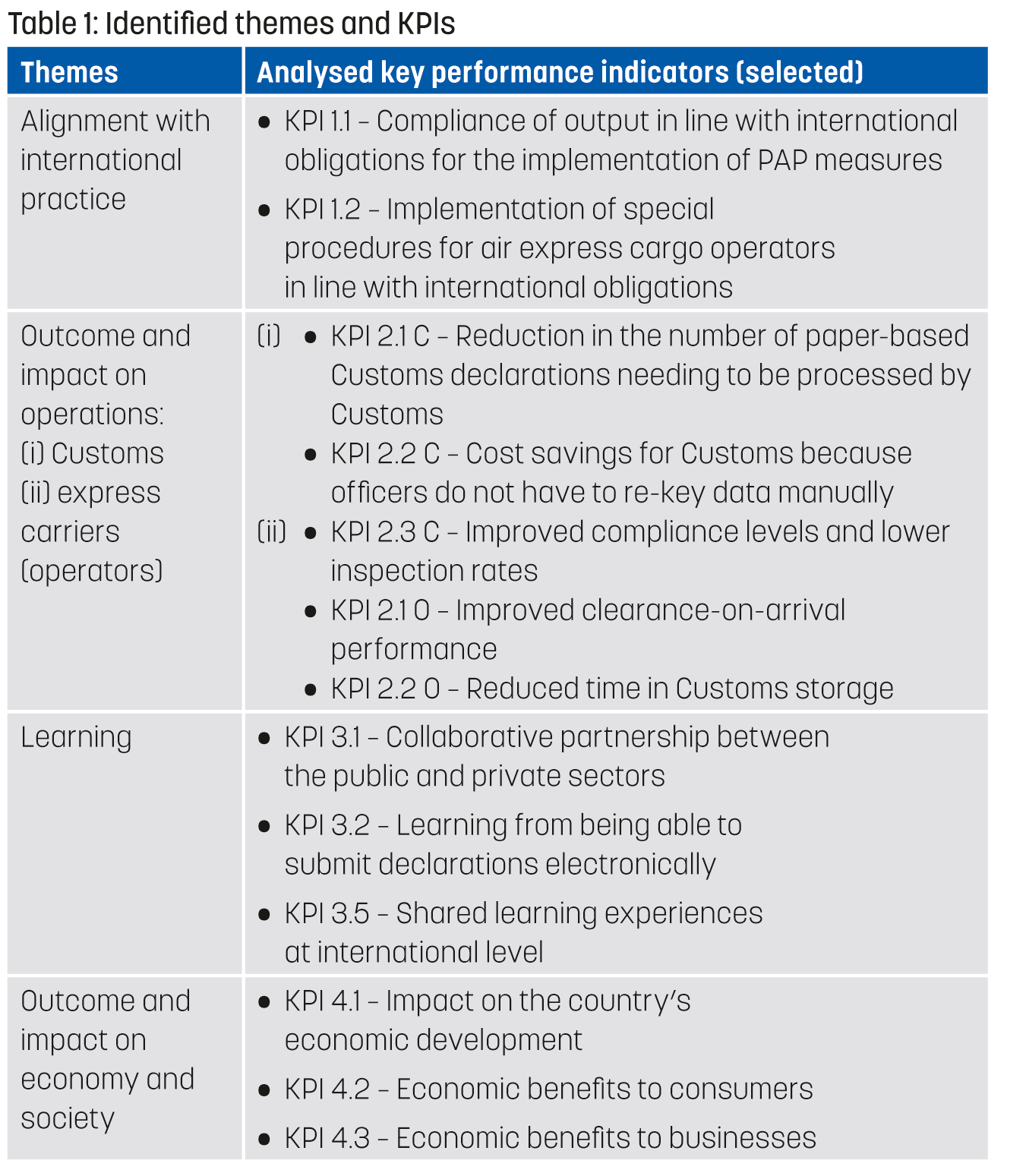

The focus of the impact assessment was on analysing the various stakeholders’ needs and available data (both quantitative and qualitative) as well as identifying any useful performance indicators that lend themselves particularly well for application elsewhere. It thus served a dual purpose: acquiring a broader and deeper understanding of the results and developing a methodology that could have other applications. Multiple iterative evaluation cycles with key project partners revealed four main themes and a corresponding set of key performance indicators (Table 1).

The impact assessment identified additional quantitative KPIs, in addition to the clearance-on-arrival rate, as follows:

Insights into the MCA’s more strategic objectives based on the four main themes identified can be summarized as follows:

What was observed, however, was that the demonstration and learning effects have an impact that reaches far beyond the new PAP capabilities. The illustrative utility of such a system encourages support for trade facilitation efforts worldwide. The approach has already been emulated by four countries in the region and is being implemented on a larger scale worldwide.

Implications for Customs performance measurement?

Drawing on a methodology first presented at PICARD 2017,[6] the approach of the impact assessment complements prevailing evaluation methodologies in trade facilitation where the focus often tends to be limited to factors such as time and costs[7] or remain fixed on more extensive macro-economic modelling.[8]

The results show that taking a closer look at the needs of stakeholders can yield additional insights that may be used to inform the debate on Customs performance measurement. Two related considerations that could be explored further are:

In the case of Montenegro, the iterative approach, using stakeholder needs analysis from which to derive KPIs and the dialogue that emerged as a result of identifying these KPIs, was highly effective, mainly due to the openness and supportiveness of the stakeholders involved.

More information

grainger@tradefacilitation.co.uk

karl.bartels@giz.de

s.pope@dpdhl.com

[1] MCA indicated a rate of 65% in 2019 (probably calculated by excluding goods subject to import requirements that are not eligible for the PAP procedure).

[2] https://www.tfafacility.org/article-7

[3] https://eur-lex.europa.eu/legal-content/EN/TXT/?uri=celex:32013R0952

[4] http://www.wcoomd.org/en/topics/facilitation/instrument-and-tools/conventions/pf_revised_kyoto_conv/kyoto_new/gach3.aspx

[5] DPDHL, Sustainability Report: “Connecting people, improving lives”. 2019, Deutsche Post DHL Group: Bonn.

[6] Grainger, A. and D. Shaw, A method for measuring trade facilitation. WCO News, 2018(85): pp. 21-23, https://mag.wcoomd.org/magazine/wco-news-85/method-measuring-trade-facilitation

[7] For example: MCA, Montenegro Time Release Study 2016, Ministry of Finance and Customs Administration, 2016, Government of Montenegro.

[8] For example: Sourdin, P. and R. Pomfret, Trade Facilitation: Defining, Measuring, Explaining and Reducing the Cost of International Trade. 2012, Cheltenham: Edward Elgar.